[ad_1]

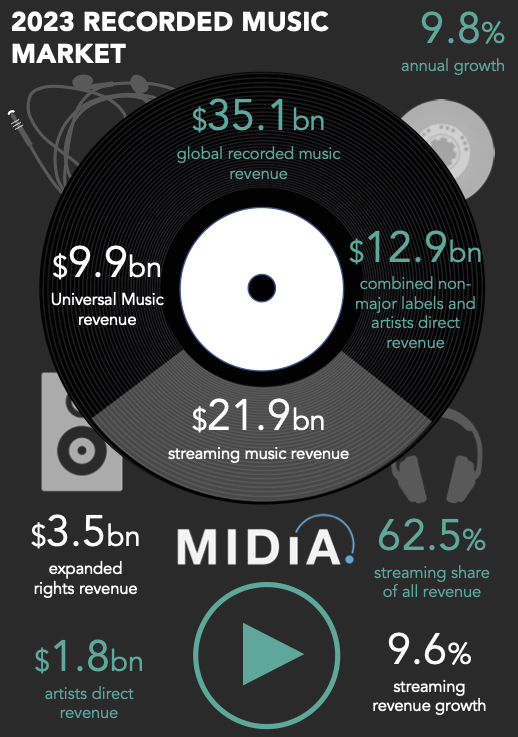

Progress is again! After a slower 2022, world recorded music revenues grew by 9.8% in 2023 to achieve $35.1 billion, in comparison with 7.1% in 2022, which signifies that the market is now greater than double (124.5%) the scale it was in 2015. 2023 was the yr during which the trade settled again right into a optimistic development trajectory after the volatility of the pandemic and post-pandemic years. However the numbers additionally level to a market that’s embarking on a significant interval of change.

The recorded music market is changing into extra diversified, and though streaming remains to be the centre piece, its function is lessening. Streaming revenues hit $21.9 billion in 2023, up a comparatively modest 9.6% on 2022. For the primary time ever, streaming grew slower than the entire market, to the extent that its share of whole revenues truly fell (to 62.5%). Apparently, over the identical interval, the 5 publicly traded DSPs grew income by 15.9%, and Warner and Sony collectively grew music publishing streaming income by 18.4%. Worth is starting to shift throughout the streaming worth chain.

In different years, the recorded music streaming slowdown would have been trigger for concern, however not in 2023. It’s because different codecs picked up the slack. Bodily, after a decline in 2022, was up once more (4.6%) in 2023, as was ‘different’. Apparently, bodily is rising because the trade kingmaker: up to now on this decade, over every of the 2 years that bodily revenues grew, trade income development was robust, and within the two years bodily fell, trade development was sluggish. Bodily is the distinction between good and nice.

The expansion in bodily revenues, nonetheless, is greater than only a income story, it displays an trade strategic shift. Anticipating the streaming slowdown, labels and artists alike have been on the lookout for diversification and new development drivers, with superfans rising because the central goal. The robust development of bodily and ‘different’ revenues in 2023 are the primary fruits of the brand new superfan focus.

Probably the most compelling proof for the superfan shift, is expanded rights. A subcategory of ‘different’, expanded rights replicate labels’ income from sources akin to merchandise and branding. Briefly: superfan codecs. Historically, expanded rights are usually not tracked as a part of recorded music trade revenues, however final yr, due to the trade’s rising fandom focus, we determined we needed to embrace them, even when different entities nonetheless don’t. 2023 underscored the significance of that call. Expanded rights income grew by 15.5% to hit $3.5 billion – 10% of all world revenues. Expanded rights are one of many predominant constructing blocks of tomorrow’s music enterprise.

Change was not constrained to codecs. Market shares took some attention-grabbing turns, too. Non-major labels had an awesome yr (and we’re calling them that, fairly than independents, as a result of a whole lot of the larger ‘independents’, akin to HYBE, have little in frequent with what folks consider as conventional indies). Non-majors grew revenues by 13.0% in 2023, in comparison with 9% for the main labels. This meant that non-major label market share was up for the fourth consecutive yr, reaching 31.5%. (Although, be aware this is measured on a distribution foundation, not an possession foundation. Subsequently, unbiased income that’s distributed through a significant file label or a completely owned main label distributor will seem within the income of the respective main file label. So ‘precise’ non-major share is greater).

Non-major labels had an awesome yr in expanded rights, outgrowing the market, largely due to Korean labels, which accounted for almost 70% of non-major label expanded rights income.

In stark distinction, 2023 was a tricky yr for artists direct (i.e., self-releasing artists), with numerous streaming market developments seeing them develop streaming income and their variety of streams far more slowly than in earlier years. 2023 was the primary yr artists direct misplaced market share. Streaming income grew simply 3.9% in 2023, in comparison with 17.9% in 2022 and 35.5% in 2021. The consequence was a 0.4 level decline in streaming market share. Regardless of a troublesome 2023, artists direct income in 2023 was 57.7% greater than in 2020, although the upcoming streaming royalty modifications will possible see development sluggish additional.

On the majors’ facet of the equation, Common remained the most important label group, with its $10.0 billion representing 28.3% market share, however for the primary time since 2020, Sony was the quickest rising main, growing revenues by 11.6%, rising market share 0.3 factors to twenty.3%

Concluding ideas

2023 was a really optimistic yr, and it could show to be the one we glance again upon as ‘when issues began to vary’. Streaming development slowed, on the recordings facet of the equation, a minimum of; monetising fandom turned a severe a part of the trade; non-majors locked into long-term market share development; and self-releasing artists began to see a transparent divergence between what they streamed and what they earned.

The trade is starting to bifurcate between the standard, streaming-focused enterprise, and a brand new one during which fandom and creation will take centre stage. Welcome to the primary yr of tomorrow’s music enterprise.

[ad_2]